How to Send Stablecoin 2026 guideline

Sending money internationally is still more complicated than it should be. Fees can stack up, delivery times can be unclear, and both individuals and businesses often deal with extra steps just to complete one transfer. With global remittance flows estimated at around $905B in 20241, it’s clear cross-border money movement has become a daily need.

Why international transfers still feel difficult

Even today, many international transfers run through multiple intermediaries, which creates four common problems:

High costs: Fees plus FX margin can add up fast. The World Bank’s tracking shows the global average remittance cost still sits around the 6% range, with many corridors remaining expensive.

Slow speed: Transfers can take hours to days depending on rails and cut-off times.

Uncertainty: Tracking and status visibility isn’t always clear end-to-end.

Access issues: Receiving money can be hard if recipients are underbanked or need cash-out options.

These issues affect everyone—individuals sending money to family, and businesses paying overseas vendors.

Why stablecoins can be a better way to move money globally

Stablecoins like USDC are designed to maintain a stable value while moving on blockchain networks. That matters because blockchain settlement can reduce the number of steps needed to move value across borders.

In practical terms, stablecoin-based flows can offer faster settlement with less dependency on banking hours, lower total costs especially for frequent transfers, more transparency which transactions are trackable, broader accessibility even with the market with limited bank services.

This is also why stablecoins show up in broader conversations about improving cross-border payments, where the systemic goals are still improving cost, speed, access, and transparency.

Stablecoin remittance benefits

If you’re comparing stablecoins vs traditional remittance rails, most people care about five things:

- Speed: less waiting, fewer manual steps

- Cost efficiency: fewer intermediaries and lower overhead

- Transparency: easier tracking and confirmation

- Accessibility: more ways to send/receive across regions

- Stability: less volatility than typical crypto assets

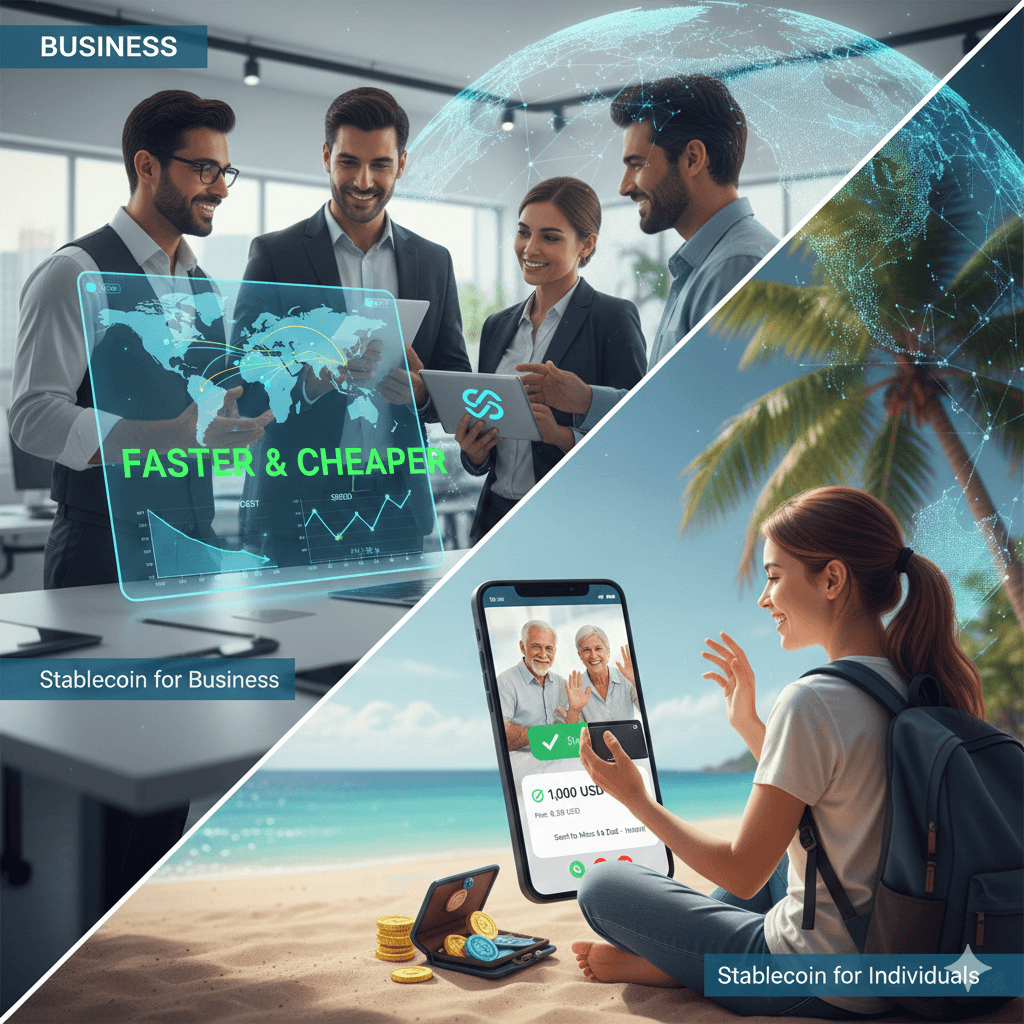

For businesses

With OwlPay Harbor, businesses can use stablecoin rails as part of a compliant on/off-ramp flow to move between local currency and USDC, then complete cross-border payouts to recipients’ bank accounts (including local-currency payouts where supported).

In a typical vendor-payment scenario, a business initiates a payout through Harbor, funds are converted from local currency into a stablecoin settlement layer, transferred across borders, and then converted back into local currency for delivery into the recipient’s bank account. This reduces operational friction and can make international payouts faster, more trackable, and easier to reconcile.

For individuals

With OwlPay Wallet Pro, users can send value using blockchain rails while the recipient receives funds in bank account, so the recipient doesn’t need to manage a crypto wallet just to get paid. If someone needs to send money abroad, they can obtain USDC inside OwlPay Wallet Pro and send funds directly to an international bank account through a simplified flow.

Real-world example

One international logistics company we worked with ran cross-border payouts to overseas vendors on a regular schedule. Before adopting Harbor, a typical payout batch took 3 business days to settle end-to-end, and the company paid an average all-in cost of 10% per payout (fees plus FX spread). After switching to a stablecoin-based settlement flow through Harbor, the same payout cycle was completed in about 2 hours, improving transfer time by roughly 90%. The team also reduced reconciliation effort by several hours per week by consolidating payout tracking and reporting.