Two Rooms, One Settlement Layer

What 25,000 industry leaders across Asia and U.S. told us about the next phase of stablecoin payments

TLDR

- Money20/20 Asia and Consensus Miami audiences are asking the same question from opposite ends of the stack: how fiat and stablecoin rails actually connect, under licensing, across borders.

- OwlPay Harbor has live settlement corridors across 22 destination countries, with 45% landing domestically in the US and 40% crossing borders into 21 foreign markets.

- Nearly two in three cross-border transactions reach Asia (led by China, the UAE, and Hong Kong). Over 80% of cross-border activity settles outside G10 financial centers.

- Monthly volume has roughly doubled within a single quarter, with one orchestration layer now serving treasury through remittance flows on the same regulated stack.

For two weeks this spring, the OwlPay team worked from booths six thousand miles apart. The first was at the Queen Sirikit National Convention Center in Bangkok for Money20/20 Asia, which closed its third edition on 23 April with over 4,500 attendees from 90 countries. The second was at the Miami Beach Convention Center for Consensus 2026, which gathered 20,000 leaders from more than 100 countries between 5 and 7 May. Between them, those two rooms contained much of the population that will determine how money moves over the next decade.

What we expected to find was a sharp contrast between the two continents. What we actually found was the same question being asked in two different vocabularies.

In Bangkok, a head of payments at a regional bank described a familiar frustration. Their customers wanted faster, cheaper cross-border settlement into and out of Southeast Asia, and stablecoin rails seemed like a credible answer, but the bank could not become a digital asset business to use them. Two weeks later in Miami, a builder described the inverse problem. They had abundant on-chain liquidity in USDC, but their treasury team would not permit local payout exposure across twenty different banking relationships. They needed a licensed counterparty who could deliver fiat to a beneficiary in Lagos, Dubai, or Manila without them having to register as a money transmitter in each jurisdiction themselves.

The two complaints describe the same gap. One side of the room has stablecoin liquidity and needs access to licensed fiat. The other side has licensed fiat reach and needs stablecoin-native rails. The settlement layer that connects those two halves is where the next decade of payments will be built, and it is the layer OwlPay has spent years constructing.

What we are actually moving

Across OwlPay Harbor, settlement activity has been building since January. Monthly volume has expanded with a roughly twofold ramp inside a single quarter, and May is still incomplete at the time of writing.

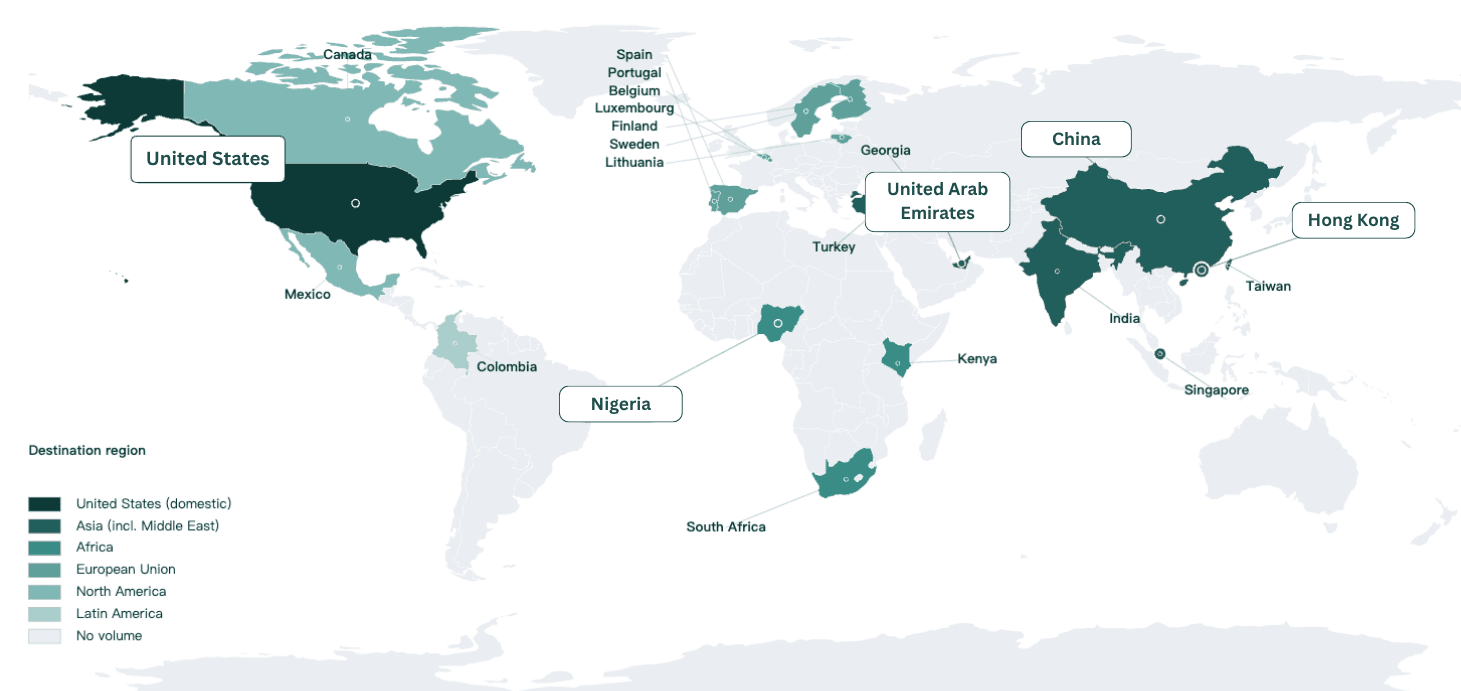

The geographic distribution of that volume is where the Bangkok and Miami conversations converge. Of the total outbound flow, 45% settled domestically inside the United States and 40% settled cross-border across 21 foreign destinations. (Note: the remaining settled on-chain or recognized as internal movements). Within cross-border activity, 63% of total transactions reached Asia (dominated by China, UAE, and Hong Kong), Africa absorbed 18% of cross-border transactions, almost entirely through the United States to Nigeria corridor. The European Union accounted for 11.5%, North America for 5%, and Latin America for 2.5%

OwlPay Harbor cross-border payout regions by transaction count

OwlPay Harbor cross-border payout regions by transaction count

OwlPay Harbor payout destination map

OwlPay Harbor payout destination map

Read together, those numbers tell a clear story about where stablecoin-enabled settlement is finding real demand. Nearly two in three cross-border transactions we settle reach Asia, and once Africa is added in, over 80% of cross-border activity is settling outside G10 financial centers. This is not a thesis about emerging markets. It is what happened in our books over the past few months.

How the rails break down

Circle Payments Network (CPN) has become our highest-frequency rail. Of all transactions, 53% settled through CPN, a growing network of regulated payout partners across major corridors in Asia, the Middle East, Europe, and the Americas. The typical CPN ticket places the rail squarely in mid-market commercial use rather than retail remittance.

Conventional wire transfers, domestic and international combined, anchor the high-ticket end of the book, typically treasury-grade and institutional B2B settlement. Real-time payments cover lower-ticket commercial flows, ACH handles small-ticket recurring movement, and debit card (enabled by Visa Direct) sits at the retail end, covering the long tail of small, fast US flows.

This combination is what makes the network durable. A single orchestration layer is serving treasury-grade institutional settlement, mid-market commercial flow, and retail-scale payouts, all on the same regulated stack, covering a range that few networks operate end-to-end on one integration.

Who is using the rails

Spark Tech is one of our key clients. Their payment service Oneremit offers fast international payments from Africa to the world, handling cross-border settlements between businesses and their clients, suppliers, and vendors. Spark Tech’s flow runs across multiple destination countries on different settlement rails, demonstrating that the same orchestration layer can support institutional-grade B2B settlement at home and cross-border payouts into emerging markets on a single integration.

Graph, operated by Oval Technologies, handles trade payments between African enterprises and their US counterparties, with payouts reaching a dozen destination countries across Asia, Europe, Africa, and the Middle East. Their pattern is mid-frequency, mid-ticket cross-border commercial flow, which is precisely the CPN sweet spot.

Hope for Haiti uses the network as a regulated on-ramp for donor capital. The organization moved over 100,000 USD into USDC, with up to 93% savings in transfer costs versus traditional channels. For an NPO working in a fragile-currency environment, that conversion is consequential. The cost of donor capital reaching the field falls when conversion is fast, regulated, and traceable.

ATM Tokens represent a P2P service provider relationship currently in the early-volume stage. Dexpay, which delivers cross-border payment flows primarily through telecommunications networks, sits in our ecosystem as a partner exploring integrated stablecoin payout flows.

Two rooms, one answer

For the fintech and payments executives in Bangkok, the Asia corridor numbers are not abstract. They are the corridors that those executives operate in every day. High-value commercial flow into the United Arab Emirates, Hong Kong, and China is the trade-weighted reality of how cross-border commerce moves through their region. What OwlPay* offers them is a regulated counterparty that already runs those corridors at scale, with Money Transmitter Licenses across 40 US states, Circle Payments Network and Visa Direct integrations, and a Nasdaq listing behind the balance sheet. They can use stablecoin settlement without having to become a digital asset business themselves.

(* All money transmission services in the United States are provided by OwlTing USA, Inc. (NMLS ID: 2324336), a wholly owned subsidiary of OBOOK Holdings Inc., under the operating brand of OwlTing’s OwlPay payment arm. For a list of U.S. licenses obtained, please see https://www.owlting.com/owlpay/licenses?lang=en.)

For the capital markets and institutional leaders in Miami, the same dataset reads as proof of reach. Over 100 destination countries on a single integration. A regulated counterparty with active settlement flow already in production. A license stack that leaves their compliance team the peace of mind in one decision rather than twenty. What OwlPay offers them is the freedom to focus on what they do well, which is creating and circulating stablecoin liquidity, without having to build out local payout infrastructure for every market they want to reach.

What this means

Stablecoin payments crossed a threshold this year. The conversation is no longer about whether stablecoins will play a role in cross-border settlement. It is about which infrastructure layer will mediate that role at scale. Issuers will create and redeem. Banks and processors will integrate and distribute. Networks such as Circle Payments Network will route value between counterparties. What has lagged is the licensed orchestration layer that sits above those networks. The layer combines CPN's payout reach with the wider toolbox of on- and off-ramps surrounding it: Visa Direct for debit card payouts, real-time payments, wire, and ACH, under a single regulated stack with the standing to operate across jurisdictions and the technical reach to serve commercial and remittance flows from one integration.

OwlPay's claim to that position is not aspirational. The transaction record substantiates it. An active settlement footprint across 22 destination countries. A U.S. State Money Transmitter License footprint covering 40 states with active applications in additional jurisdictions. A client roster spanning humanitarian capital, institutional B2B commerce, fintech payment service providers, and beyond.

Demand for that orchestration layer is now showing up at a pace. According to the latest earnings release*, we have had 36 enterprise clients with executed commercial agreements, up from more than 20 clients reported on March 31, 2026, with aggregate annual payment volume across these clients' own existing businesses growing from over US$5 billion to over US$6 billion. Contracted client momentum and corridor activity continue building through Q2 2026. The new mix of signed names continues to span, and that breadth is the strongest read we have that no single buyer segment has cornered it yet. Bangkok and Miami were asking the same question from opposite ends of the room. The value of a connected settlement layer has emerged.

(* According to OwlTing’s press release, “OBOOK Holdings Inc. Announces Financial Results for the Full Year 2025 Ended December 31, 2025,” announced on April 29, 2026. Please see https://www.globenewswire.com/news-release/2026/04/29/3284305/0/en/obook-holdings-inc-announces-financial-results-for-the-full-year-2025-ended-december-31-2025.html)

About OwlTing Group

OwlTing Group (NASDAQ: OWLS) is the operating brand of OBOOK Holdings Inc., a blockchain technology company founded in Taiwan, with subsidiaries in the United States, Japan, Poland, Singapore, Hong Kong, Thailand, and Malaysia. The Company operates a diversified ecosystem across payments, hospitality, and e-commerce. In 2026, OwlTing was named to the Financial Times and Statista “High-Growth Companies Asia-Pacific 2026” list, ranking No. 226 among the top 500 fastest-growing companies in the region with a 42% CAGR. In 2025, OwlTing was ranked among the top 2 global players in the "Enterprise & B2B" category by CB Insights' Stablecoin Market Map. The Company’s mission is to use blockchain technology to provide businesses with more reliable and transparent data management, to reinvent the global flow of funds for businesses and consumers, and to lead the digital transformation of business operations. To this end, the Company introduced OwlPay, a Web2 and Web3 hybrid payment solution, to empower global businesses to operate confidently in the expanding stablecoin economy. For more information, visit https://www.owlting.com/portal/?lang=en.

Forward-Looking Statements

This article contains forward-looking statements within the meaning of applicable securities laws. These statements relate to future events or the Company’s future financial or operating performance and involve known and unknown risks and uncertainties that may cause actual results to differ materially from those expressed or implied by such statements. Forward-looking statements can often be identified by words such as “may,” “will,” “expect,” “anticipate,” “plan,” “intend,” “believe,” “estimate,” or similar expressions. These forward-looking statements are based on the Company’s current expectations and assumptions and speak only as of the date of this announcement. The Company undertakes no obligation to update any forward-looking statements, except as required by law. Investors are cautioned not to place undue reliance on these statements and are encouraged to review the risk factors described in the Company’s filings with the U.S. Securities and Exchange Commission.

Digital Asset and Blockchain Disclaimer

References in this article to digital assets, blockchain technologies, stablecoins, or distributed ledger technology are for informational purposes only and do not constitute an offer to sell or a solicitation of an offer to buy any digital asset, security, or financial instrument. Digital asset markets are subject to significant volatility and regulatory uncertainty, and the availability of related products and services may be subject to regulatory approvals and compliance with applicable laws and regulations.

Third-Party Information

This article may contain references to third-party companies, products, services, or research publications. Such references are provided for informational purposes only and do not constitute an endorsement, sponsorship, or recommendation by the Company unless expressly stated.